Stablecoins: Unlocking Fintech's Next Frontier

While the transformative capabilities of stablecoins are widely acknowledged and often framed by their underlying technological stack (issuance, orchestration, distribution, and applications), we explore the potential opportunities from a different angle. This article views stablecoins as the next generation of fintech, examining how they are uniquely positioned to penetrate and succeed in markets still largely untouched by existing fintech players.

To understand this evolving landscape, the BCG and QED Global Fintech 2025 Report provides valuable insights, illustrating how fintech's journey from challenger to incumbent has reshaped consumer banking and payments over the last decade. This first wave of fintech, which we will term Fintech 1.0, includes familiar names like Stripe (payments), Revolut (neobank), Venmo (digital wallet), and Klarna (BNPL).

Crucially, the report maps where fintech has succeeded, stalled, and, most importantly, where meaningful gaps persist across 1) geographical regions and 2) product categories.

These underserved areas, in our view, represent the true next frontier - a compelling opportunity for stablecoin-native companies to innovate, build, and achieve significant scale.

1. Stablecoins as the Global Fintech Infrastructure

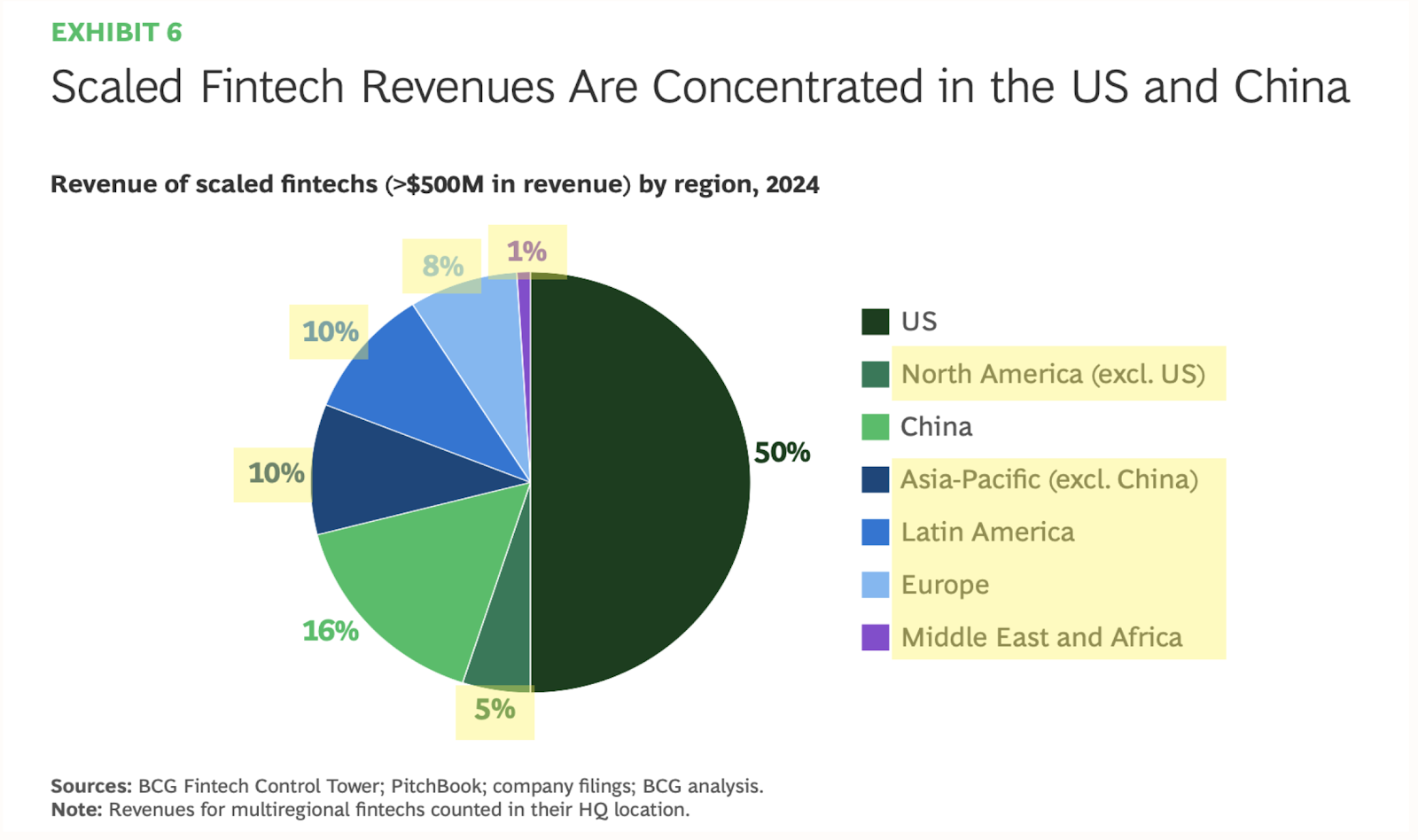

Fintech 1.0 created significant enterprise value, especially in developed markets. As Figure 1 shows, over 70% of fintech’s success was concentrated in the US, China, and parts of Western Europe, where digital infrastructure and consumer demand were relatively mature.

This concentration in developed markets left significant gaps in underserved regions (Figure 1, highlighted in yellow), including Latin America, Middle East & Africa, Mexico, and emerging European and APAC markets (e.g., Southeast Asia, Turkey, Ukraine). These ecosystems, lacking modern banking rails and burdened by high fees and slow traditional systems, have proven to be fertile ground for stablecoin fintechs.

For instance, a Fireblocks survey reveals 71% of Latin American respondents already use stablecoins for cross-border payments, double that of North Americans. Similarly, Chuk Okpalugo emphasises stablecoins' transformative role for financial services in Africa.

These dynamics reveal a significant untapped opportunity for stablecoin-native solutions to address long-standing gaps in these regions.

2. Stablecoin as Fintech 2.0: The White Space Ahead

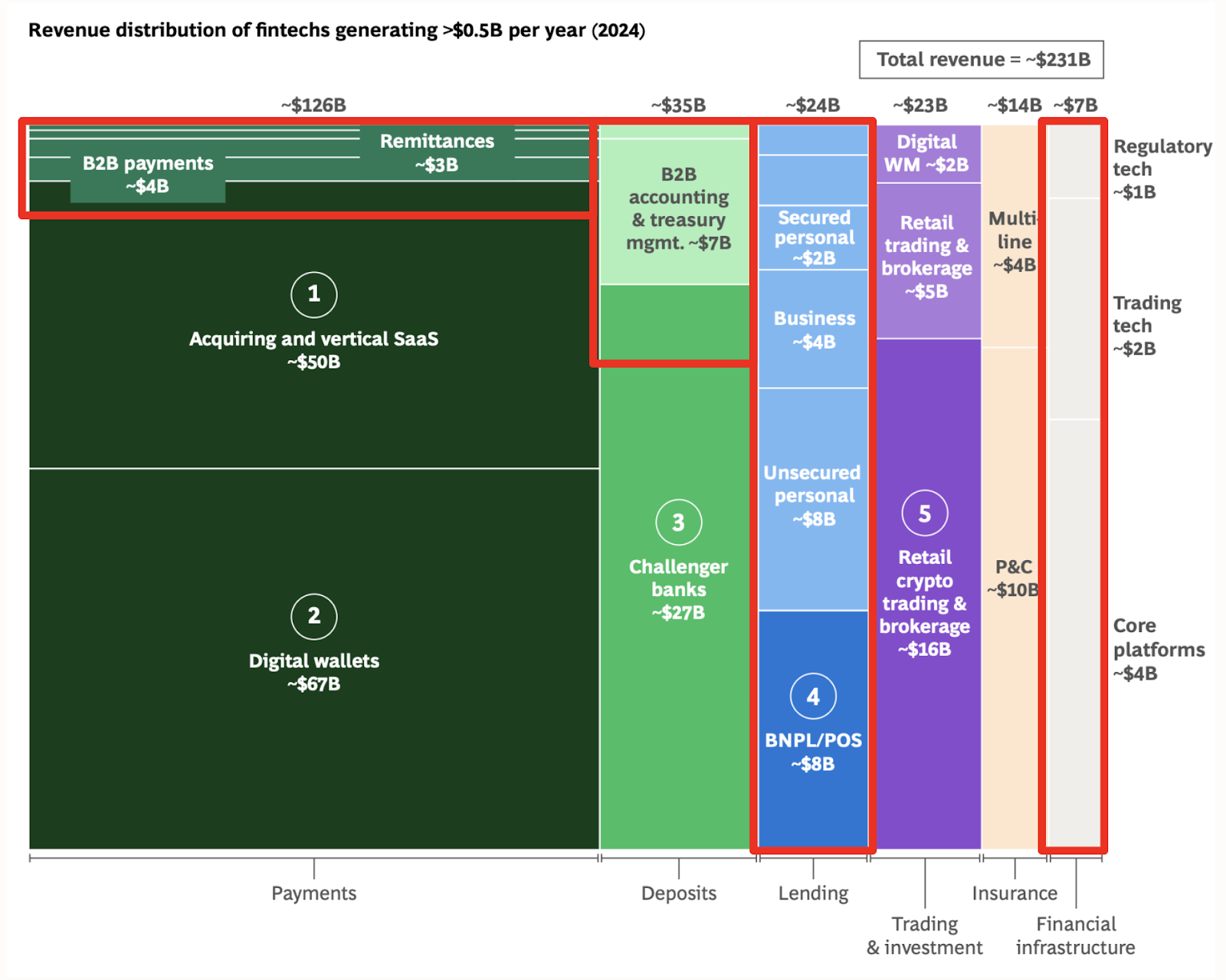

While underserved regions offer untapped geographical markets, a distinct 'white space' lies in product categories beyond Fintech 1.0's reach. Here, structural constraints (fragmented settlement and capital, regulatory complexity) limited Fintech 1.0's traction, presenting new opportunities for stablecoin-centric solutions.

Viewed through this lens, four domains (Figure 2, outlined in red) constitute prime territory for stablecoin fintechs to introduce new primitives, resolve systemic bottlenecks, and capture differentiated revenue.

They can be grouped into:

A) B2B Payments and Remittances

B) B2B Challenger Banks and Treasury Management Platforms

C) Credit and Lending Platforms

D) Financial Infrastructure & Enablers

A) B2B Payments and Remittances

There is already a clear product market fit for this use case, with stablecoins significantly improving settlement speed and reducing costs in global commerce and remittance flows. Early leaders like BVNK are already serving over $10 billion in annualised volume and are rapidly expanding their product suite.

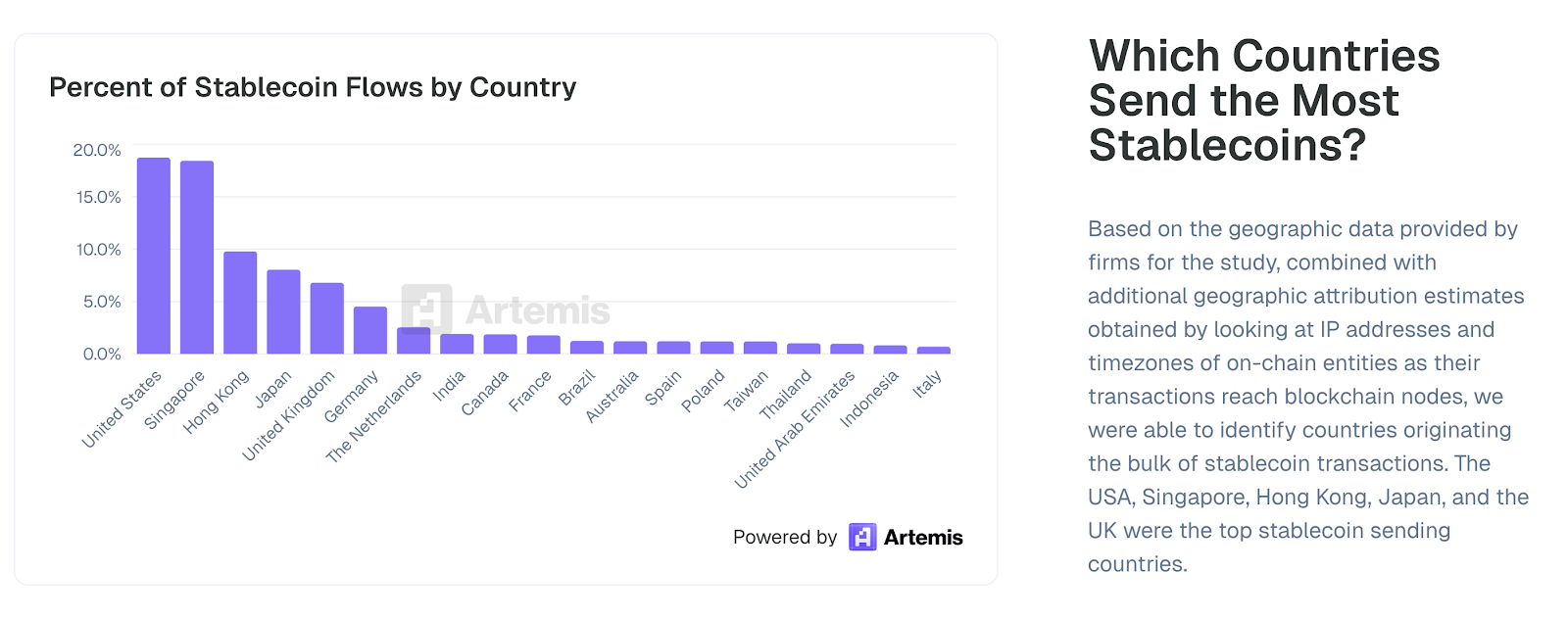

However, there is significant room for regional challengers, especially in Asia. Artemis recently reported that more than 30% of stablecoin flows originate from Singapore and Hong Kong (see Figure 3), underscoring their role as key hubs with robust financial infrastructure. This opportunity is amplified by the fact that Asian clients often prefer providers with a strong local presence and specific product requirements tailored to regional nuances.

Obita (Mirana portco), founded by senior executives from Hashkey and Ant Financial, is a strong contender to build the leading stablecoin payments company in Asia, leveraging their deep regional expertise and industry relationships. These dynamics highlight B2B payments and remittances as a critical and rapidly evolving space for stablecoin innovation and adoption, particularly within the diverse emerging markets.

B) B2B Challenger Banks and Treasury Management Platforms

In Fintech 1.0, Mercury became a category-defining product by layering a modern banking experience on top of traditional rails. It has scaled tremendously and raised $300 million at a $3.5 billion valuation in 2025. With $500 million in revenue (2024), its core clients include international startup founders, SaaS companies, freelancers, and crypto-adjacent businesses. Notably, these clients seek easy access to USD banking services and significantly overlap with early adopters of stablecoins.

With stablecoins offering a superior form of USD access, stablecoin-native alternatives are fast emerging:

- Dakota is the closest analogue: a non-custodial platform offering stablecoin-backed business accounts, treasury tools, and payments.

- Singapore Gulf Bank (Mirana portco), backed by Bahrain's sovereign wealth fund Mumtalakat and Singapore-based Whampoa Group, is the first fully licensed stablecoin-native bank in the MENA region - offering real-time, multi-currency clearing and other digital asset-integrated services for corporate clients.

- Erebor, backed by industry heavyweights like Palmer Luckey and 8VC (Joe Lonsdale, founder of Palantir), takes a more ambitious path, applying for a US national bank charter to become the first fully licensed, stablecoin-native bank.

There is still significant room for growth. USD demand remains high in markets where banking access is constrained and treasury management services remain underdeveloped, requiring many more essential building blocks.

Among these, Plasma (Mirana portco), the leading purpose-built stablecoin chain, offers features like zero-fee transfers and confidential payments. Additionally, Multiliquid is building infrastructure for 24/7 exchange of blue-chip real-world assets (RWAs) and stablecoins, across multiple blockchains and at scale.

More opportunities will surface as both stablecoins and AI redefine the CFO stack through intelligent automation, real-time insights, and new financial instruments.

C) Credit and Lending Platforms

Stablecoins offer the potential for a global, programmable credit market. However, current DeFi lending falls short for real-world businesses due to overcollateralization and a fundamental lack of off-chain creditworthiness assessment. This creates a significant gap in an eager market, representing a substantial "white space" opportunity.

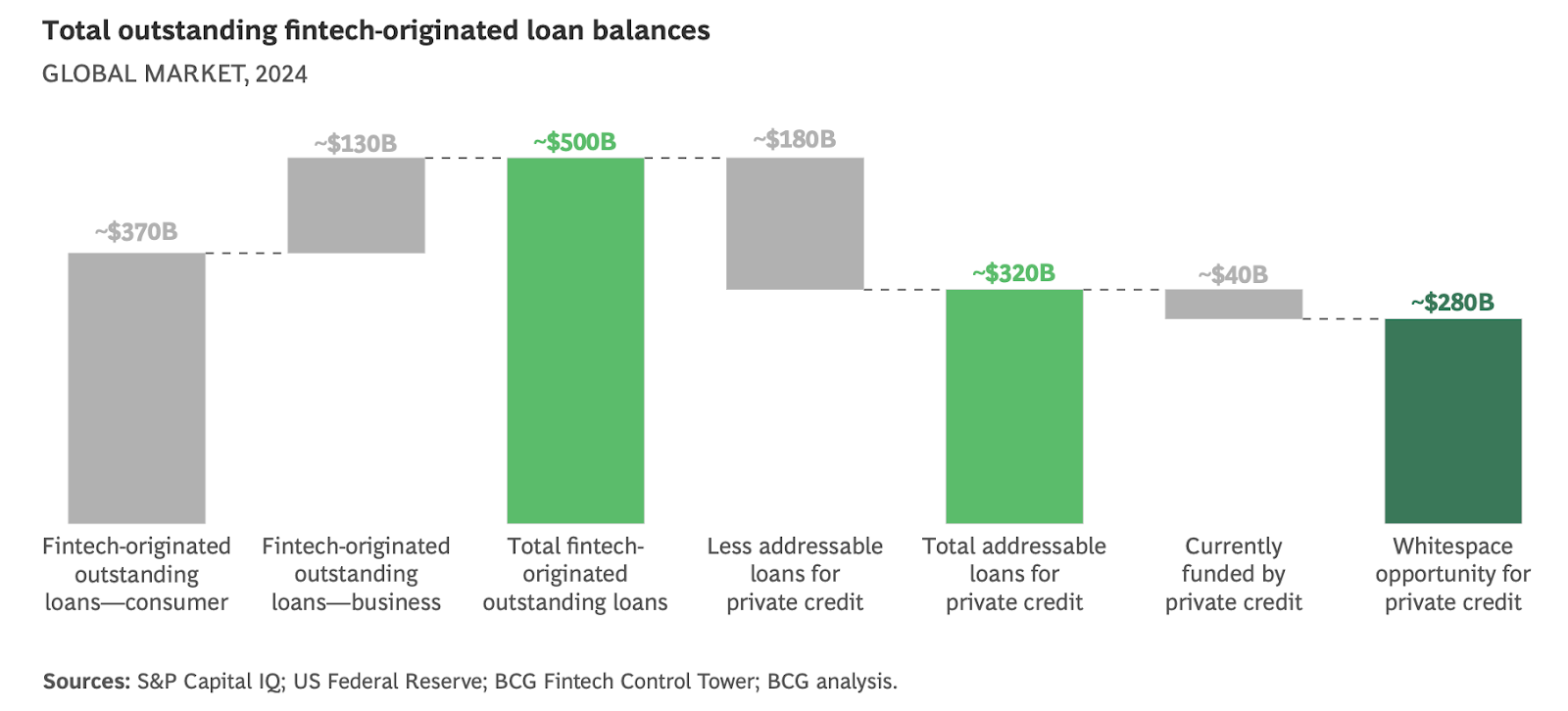

One potential opportunity lies in plugging the immense friction and funding gap present in Fintech Lending. While Fintech Lenders (BNPL, earned wage access, or embedded B2B lending) excel at customer acquisition and loan origination, they struggle with funding - often relying on expensive equity capital, bank partnerships, or increasingly private credit. The BCG and QED Global Fintech 2025 report (Figure 4) identifies a $280 billion gap in funding for fintech lending, with a projected CAGR of 42%. While private credit has shown a growing appetite, securing a facility remains an onerous process that can take up to 6 months, severely limiting lenders' growth.

The rapidly growing stablecoin pools on both decentralised and centralised finance offer a compelling and superior capital engine. As Simon Taylor astutely observes, stablecoins are not merely cheaper rails for money transfers; their power lies in their inherent programmability, global accessibility, and 24/7, real-time settlement capabilities. Tapping into global stablecoin pools on DeFi as a faster, more flexible, and automated capital backend would enable fintech lenders to bypass the slow and rigid traditional credit facilities.

Opportunities here are plenty, ranging from new, global fintech lenders powered by stablecoin pools to on-chain asset managers that allocate capital across these lenders. Evidence of this is already appearing: Galaxy Research, for instance, notes that stablecoin issuers are already significant non-bank lenders, and “vault” products like Ethena (Mirana portco) have already opened the Overton window for dollar-denominated yield sources on-chain.

We are actively exploring these and other opportunities to architect the future of on-chain credit broadly.

D) Financial Infrastructure & Enablers

To truly unlock stablecoin-native financial products at scale, the ecosystem requires foundational infrastructure that abstracts complexity, ensures trust, and enables seamless composability across borders and asset types.

Interoperability networks like Mesh (Mirana portco), which securely connect hundreds of exchanges, wallets, and payment service providers, play a pivotal role.

Clearing networks, such as Ubyx and Atum (both Mirana portco), are driving the industry forward by enabling seamless acceptance and redemption of all stablecoins through regulated financial channels, helping stablecoins meet the test for singleness of money. Building on insights from Ubyx’s excellent whitepaper, four key enabler categories are crucial for facilitating the next wave of financial innovation:

- Core Systems and Data Integration: Seamless integration with existing institutional systems (core banking, ERP, risk management) is paramount for automated reconciliation, real-time treasury management, and integrated financial reporting from on-chain activity. Stablecore is an early attempt at building this integration.

- Digital Identity and Confirmation of Payee: While much discussion has focused on the need for on-chain identity primitives, what is also needed is robust, identity-aware infrastructure. This includes advanced wallets with embedded KYC/KYB and conditional payment systems, which are necessary for scaling stablecoin usage.

- Credit and Underwriting Primitives: Existing DeFi models for global on-chain credit formation are limited by the requirement for overcollateralization and a fundamental lack of off-chain context for underwriting. Therefore, infrastructure that combines both on- and off-chain parameters, along with undercollateralized lending models, is key for unlocking the true potential of on-chain lending.

- Tokenisation Infrastructure: Infrastructure for the compliant tokenisation and distribution of diverse real-world assets (RWAs) is critical for expanding the stablecoin potential beyond digital cash into a broader tokenised economy.

Conclusion

Stablecoins are not merely a technological evolution but a fundamental reshaping of the fintech landscape, presenting opportunities to address long-standing gaps in global financial inclusion and efficiency. As infrastructure matures and adoption grows, stablecoins are poised to power the next generation of financial services.

At Mirana Ventures, we are actively partnering with pioneering founders who share this vision, with portfolio companies including: Agora, Atum, Codex, Ethena, Mesh, Obita, Pave Bank, Plasma, Singapore Gulf Bank, Ubyx, Veda, ZAR.

We welcome builders and investors interested in shaping the future of stablecoin-native fintech to connect with us!