New Financial Infrastructure: Building Blocks Worth Backing

A new class of financial infrastructure company is emerging, one that looks fundamentally different from anything the first wave of fintech produced. These companies share a common profile: their systems are real-time, global, programmable, and intelligent simultaneously. Not one or two of those properties bolted on as an afterthought, but all four architected in from the start. That convergence is what defines what we call New Financial Infrastructure.

There are already early signs that the infrastructure layer underneath financial services is being rebuilt: Mastercard acquiring stablecoin payments company BVNK, Shopify and PayPal partnering with Perplexity to launch agentic payments, and new fintechs building card issuance from scratch on stablecoin rails. These are not isolated experiments.

Our previous research mapped where Fintech 1.0 won, where it stalled, and why stablecoins are the infrastructure upgrade that gets finance to the places fintech never reached. This piece zooms out further. Stablecoins are one primitive among several driving this shift. Here, we lay out the building blocks powering the next generation of financial products, and where we see the most compelling opportunities forming.

Framing New Financial Infrastructure

New Financial Infrastructure (NFI) is our term for the emerging class of companies building the core plumbing for the next generation of financial services.

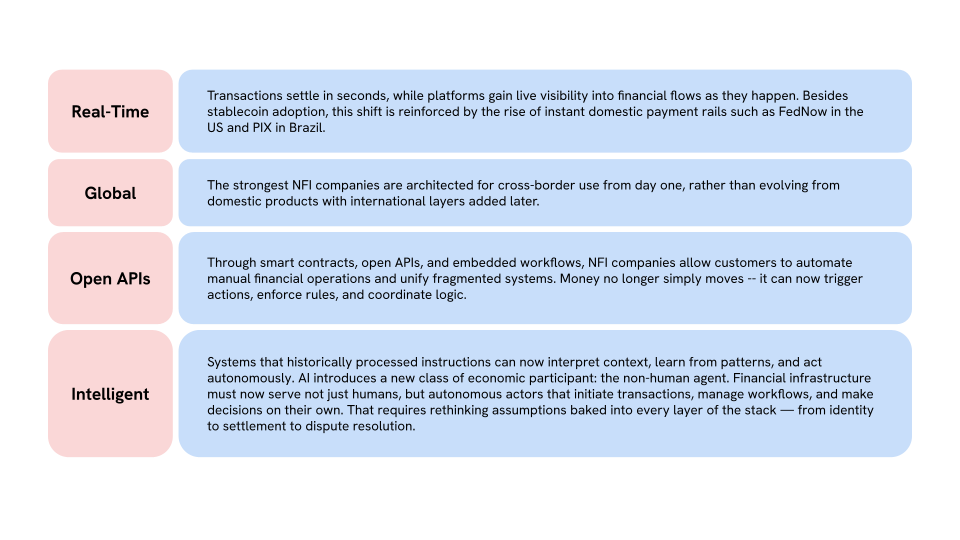

Fintech's first wave modernized legacy systems in important but often isolated ways -- making transactions faster, expanding access, digitizing workflows, or improving user experience. What defines this next wave is not any single improvement, but the simultaneous convergence of four characteristics: systems that are real-time, global, programmable, and intelligent at the same time.

This convergence is being enabled by a common set of technological primitives: stablecoins and tokenization, smart contracts, open APIs, and AI. Most NFI companies today are built on some combination of these primitives, and the most durable ones will eventually incorporate all four. The exact architecture varies by use case, but the underlying toolkit is increasingly shared across the category.

These primitives make it possible for next-generation financial services to express all four characteristics simultaneously:

Why Now

The infrastructure layer is maturing fast, driven by a convergence of forces.

Regulatory clarity. The GENIUS Act, passed in July 2025, is the first federal stablecoin framework in US history. The FDIC and OCC are finalizing implementation rules with a July 2026 deadline, putting full implementation on track for late 2026 or early 2027 -- months away now. Simultaneously, the CFPB's open banking rule took effect April 1, 2026, requiring the nation's largest banks to share customer data with third parties. These two regulations, staggered but overlapping, unlock both the supply of stablecoin-powered products and the infrastructure to distribute them.

AI-native financial services. 2026 is shaping up to be the year of AI agent adoption. 54% of organizations are now actively deploying AI agents, and 40% of enterprise applications will include task-specific agents by end of 2026 -- up from less than 5% in 2025. AI-native NFI companies natively embed agentic capabilities or build for agentic consumption from the ground up. The companies that treat agents as first-class participants in their infrastructure -- rather than bolting on AI features after the fact -- will have a structural advantage.

Stablecoin and tokenization infrastructure at scale. Stablecoins reached $316 billion in market cap by March 2026, with transaction volume of $33 trillion in 2025 -- a 72% year-over-year increase. But the opportunity extends beyond stablecoins alone. Tokenization of real-world assets -- from money market funds to equities to novel financial instruments -- is expanding the range of value that can move on programmable rails.

What makes this moment different is the simultaneity. Regulatory frameworks are finalizing, not pending. AI agent deployment is reaching mass adoption, not experimentation. And stablecoin and tokenization infrastructure has moved from niche to mainstream. For founders building NFI companies, this is the window to establish the defining platforms of the next financial era.

Where We Are Investing

Against that backdrop, here are the four areas where we are most actively investing.

1. Stablecoin Infrastructure

Stablecoin infrastructure is the base layer that makes real-time, global settlement possible. The companies here are solving the remaining gaps that prevent it from working at institutional scale -- bridging regulated finance and on-chain rails, and extending cross-border settlement beyond USD.

Stablecoins as a payments category have been extensively covered in our previous research, and with portfolio companies like Mesh and Rain leading the way, we believe there are still plenty more opportunities in this space. Here, we highlight two areas that are especially compelling at this point.

Bridging regulated institutions and on-chain rails. As more institutions look to participate in on-chain finance, a range of problems need solving: how they enter on-chain markets compliantly, how tokenized money clears and settles reliably enough to be used everywhere, and how interoperability across asset management, liquidity, and compliance systems is achieved. This also includes bringing assets on-chain -- whether existing instruments like money market funds and equities, or novel ones like tokenized trading strategies, as pioneered by our portfolio company Ethena. DigiFT gives institutions a regulated entry point into on-chain markets. Ubyx and Atum build the clearing layer that makes tokenized money interoperable across issuers and rails.

On-chain FX. As more companies and consumers move their assets and operations on-chain, they will increasingly need to transact in currencies beyond USD. Today, doing so requires off-ramping, converting through traditional FX infrastructure, and on-ramping again -- a friction-heavy process that undermines the speed and cost advantages of operating on-chain. We expect this category to expand significantly -- not just in liquidity provision across non-USD stablecoin pairs, but in hedging and structured products that were previously gated behind high AUM thresholds or prohibitive bank fees. On-chain rails can deliver those tools directly to businesses and consumers. It is still early, and no clear winner has emerged, but the underlying opportunity is clear: on-chain FX is where the real-time and global characteristics of NFI most visibly converge.

2. Agentic Commerce

When financial infrastructure becomes programmable, it opens the door to a new class of participant: autonomous agents that can initiate, evaluate, and execute transactions without human intervention. Agentic commerce is where the programmable and intelligent dimensions of NFI converge, and where the infrastructure gaps are most acute. We are most focused on the pay and transact layer.

Traditional payment systems assume either deterministic code or intentional human action. AI agents, by contrast, are probabilistic reasoning engines -- a fundamental mismatch. Without a deterministic control plane separating reasoning from execution, transaction failures and exploits become real. For pay and transact to work reliably at scale, the control layer must be built alongside it.

We see three distinct areas of opportunity within agentic payments. The clearest way to understand where they sit is to ask: who is the agent transacting with?

Agent-to-human transactions. When an agent pays a person, merchant, or business, all the compliance and identity requirements of human transactions apply. The infrastructure needed is a trust and compliance wrapper on top of existing rails: a policy engine governing what the agent can spend and with whom, wallet infrastructure, and risk and dispute management designed for non-human actors. Payman is building a bank account for AI agents that handles ACH payments and enforces spending limits. Mesh approaches the same problem from a crypto-native angle, connecting wallets, exchanges, and merchants across 300+ platforms so that AI agents can fund, route, and complete stablecoin transactions without human intervention.

Agent-to-agent transactions. When agents transact with each other, the economics and the interaction patterns shift entirely. Human commerce is episodic: a buyer decides, pays, and moves on. Machine commerce is continuous: agents negotiate, transact, and re-transact in milliseconds, often in amounts too small for traditional rails to process profitably. Card networks were designed around a $0.30-plus-2% interchange model that works for restaurant bills, not for millions of sub-cent API calls per hour. Stablecoins are a natural fit: programmable, globally addressable, and near-zero marginal cost at settlement. Natural is building in this direction, giving agents their own stablecoin wallets so that agent-to-agent payments settle instantly at micropayment scale.

Control layer. Stablecoins solve programmable settlement, but the surrounding stack does not yet exist: pre-transaction screening, standardized arbitration, chargeback equivalents for autonomous execution, and insurance frameworks tied to agent identity. When an agent executes a disputed transaction, responsibility is not yet clear -- whether it sits with the deployer, the platform, the identity provider, or the policy engine. The companies that define those standards will control the rails for autonomous commerce. Early developers will gravitate toward whichever rails are easiest to integrate and cheapest to operate.

The control layer problem in agentic payments is partly an identity problem -- and that same infrastructure gap runs across the broader NFI stack.

3. Identity and Privacy

Real-time, global, programmable systems only scale if they can verify who -- or what -- is transacting. Identity is the trust layer that makes the other three characteristics viable beyond closed ecosystems, and it remains the least mature part of the stack.

The opportunity divides cleanly into two problems: proof of credentials (can I trust who you claim to be?) and proof of creditworthiness (can I trust you with capital or risk?). These are distinct design challenges with different winners, but one cannot be solved without the other.

Proof of credentials: Verifying that a counterparty is KYC'd, jurisdiction-eligible, and sanctions-clear, without requiring repeated disclosure of raw personal data. The opportunity is in privacy-preserving verification infrastructure: systems that confirm eligibility once and carry that credential across platforms and jurisdictions without exposing the underlying data. In this way, identity becomes programmable and globally portable, expressing two of the core NFI characteristics at the trust layer.

The challenge is that verification only becomes trustworthy across platforms if it is issued by a regulated entity with genuine compliance authority. UR is building in this direction, operating as a regulated on-chain bank that issues individual IBANs and KYC credentials as on-chain NFTs. Because identity lives on-chain rather than in a centralized database, a user verified once can carry that credential across wallets, DeFi protocols, and applications without repeating the KYC process.

Proof of creditworthiness: The web2 parallels are instructive. Plaid established financial connectivity. FICO standardized the signal. Both were necessary. Together they unlocked hundreds of billions in lending. On-chain, the same two problems exist but may diverge more starkly.

Financial Connectivity: A lender cannot assess creditworthiness without seeing a borrower's full financial picture. The winner here will be determined by differentiated access to data from both on-chain and off-chain sources.

Credit Scoring: Translating that data into standardized risk signals. This is the deeper but more uncertain problem. The critical question is whether new on-chain credit standards will emerge, or whether traditional players like Moody's will successfully extend their frameworks into the on-chain economy.

Our view is that a financial system that is global, real-time, intelligent, and programmable will unlock use cases at a speed, scale, and complexity not supported by existing players. We believe new standards -- ones that start from an on-chain premise -- will emerge, and we are actively looking for the teams building them.

4. Embedded Finance

The original promise of embedded finance was that any platform could become a financial services company. In practice, the sponsor bank model constrained what was possible: batch settlement, rigid compliance frameworks, and siloed data meant that embedded products were copies of bank products distributed through software, not new financial primitives in their own right. NFI changes the terms. Stablecoins make settlement real-time. Smart contracts encode financial logic directly into the product. And because assets are tokenized on public blockchains, data and value that were previously trapped inside individual platforms become composable across them. That last point matters most: it turns embedded finance from a distribution strategy into an infrastructure category.

Within this sector, the categories we are most focused on are payments, cards, lending, and brokerage.

The clearest illustration of what changes is lending. Platforms with real-time visibility into their users’ cash flows have always been better underwriters than banks. Toast knows exactly how much a restaurant earns every night. DoorDash knows a driver’s weekly earnings to the dollar. What these platforms lacked was infrastructure with matching speed and openness: settlement that could recycle capital as fast as the data priced it, and composable rails that let financial products extend beyond a single platform’s walls. NFI provides both.

The impact is most visible in capital efficiency. On stablecoin settlement rails, repaid capital recycles immediately into the next credit facility rather than sitting idle for days on ACH. And because tokenized cash flows are composable on public blockchains, the financial products built on top of them are no longer siloed within a single platform. We are already seeing early signs of this downstream of major stablecoin card issuers like Rain.

Rhythmic is building the embedded finance platform for this transition. Consumer brands can use Rhythmic to offer stablecoin-backed stored-value accounts, co-branded cards, rewards, and lending within their own products -- without building or operating payments infrastructure themselves. It is the kind of platform that only becomes possible when composability, real-time settlement, and programmable logic are all present in the stack.

The same principle applies on the fiat side: platforms don't need to build banking infrastructure themselves to offer it to their users. Pave Bank, a licensed digital bank, offers programmable banking services to platforms like Bybit so that registered users get access to personal IBANs and cards, allowing them to manage their crypto and fiat holdings in one place.

What makes this genuinely new infrastructure is the speed of the loop: data feeds risk assessment, which generates pricing, which produces a financial product, which settles in seconds, which generates new data for the next cycle. When all four NFI characteristics are present, embedded finance becomes something qualitatively different and enables new business models that previously weren't feasible.

Conclusion

The financial system today is fragmented by geography, permission structures, and human intermediation. The four categories we have outlined -- stablecoin infrastructure, agentic commerce, identity, and embedded finance -- are each attacking a different face of that fragmentation. But the real opportunity is in their convergence.

Consider what becomes possible when these layers connect: a supply-chain finance product that underwrites using on-chain credit scores, settles in stablecoins, and extends across borders without requiring separate KYC at each node. Or an AI agent that autonomously rebalances a user’s financial position across global venues, with identity verification and dispute resolution handled at the protocol level rather than by a human compliance team.

These are not speculative. The building blocks exist today. The regulatory frameworks are finalizing. The question is which teams will assemble them first.